When I look at Microsoft right now, one image keeps coming back.

A company is standing on a construction site. Dust in the air. Mud underfoot. Steel, concrete, and unfinished roadwork everywhere. People nearby are impatient: How much more will this cost? When does the road open? Where are the cars? Where is the toll booth? Where is the cash flow?

Microsoft does not explain very much. It keeps building.

Markets rarely enjoy this kind of picture. Especially now. AI has moved past the easiest storytelling phase. Two years ago, attaching AI to a company name could add a layer of shine to the valuation. Now investors are opening the accounts. They are looking at electricity, chips, data centers, depreciation, gross margin, and one cold question:

When does the money being spent become profit?

So it is not surprising that Microsoft gets criticized.

It is big. It is visible. Azure is expanding. Copilot is being pushed across the product stack. Data centers keep absorbing capital. AI is being placed into Office, Teams, GitHub, enterprise cloud, security, and developer systems. Every item sounds futuristic. Every item is expensive.

In a bull market, expensive is called investment.

When the market gets nervous, expensive is called pressure.

That is why a simple explanation becomes tempting: AI is too capital intensive.

That sentence is not wrong. I just think it is only half of the story.

The more interesting part is the other half.

From Answers to Work

For a long time, many people looked at AI through the chat box. A user types something. A model replies. It feels like a very smart service desk, or an assistant that can be summoned at any time.

That has value. But it is not yet the deepest part of enterprise software.

Companies do not usually pay the largest amounts for beautiful answers alone. They pay when workflows actually move, permissions stay clean, data does not leak, mistakes can be investigated, costs can be controlled, employees waste less time, and the business becomes measurably faster.

That moves AI into a different place.

When AI moves from answering questions to completing tasks, the meaning of cloud changes.

An agent that actually works will not live only inside a chat window. It may need to read documents, enter databases, call tools, write code, check mail, connect to CRM, inspect calendars, follow approvals, generate reports, and be stopped before it does the wrong thing.

This does not sound romantic.

But it is exactly where enterprise software becomes valuable.

Microsoft's problem is here. Its opportunity is here too.

If AI Stays in the Chat Box

If AI remains mostly a chat interface, Microsoft's heavy investment can look clumsy. The market can argue that models can be swapped, front ends can be swapped, APIs can be swapped, and users can be swapped. In that world, building so much data center capacity and integrating so deeply into enterprise systems may turn Microsoft into a very expensive AI utility provider.

That risk is real.

If agents do not become part of daily enterprise workflows over the next few years, today's spending will look heavy. The critics will have a point. A story can be large, but without enough revenue and profit to receive it, the story eventually returns to the financial statements.

But if agents do start doing real work inside companies, the setup changes.

Companies will not casually allow a black-box AI system to roam through files.

They will not accept vague permission boundaries.

They will not tolerate agent spending that nobody can see.

They will not accept a system where, after something goes wrong, nobody can tell what happened.

At that point, intelligence is only the ticket.

The true entrance requirement is trust, control, and auditability.

Microsoft's Old Strengths Matter

Microsoft happens to be good at these old-fashioned things.

It does not only have Azure. It also has corporate email, documents, meetings, spreadsheets, code repositories, identity, permissions, security, compliance, cloud resources, and enterprise sales channels. In many companies, daily work already flows through Microsoft's pipes. Employees open Outlook, Teams, Excel, SharePoint, GitHub, and cloud systems. Behind those habits sits Microsoft's territory.

That is where I think the market may be underestimating the story.

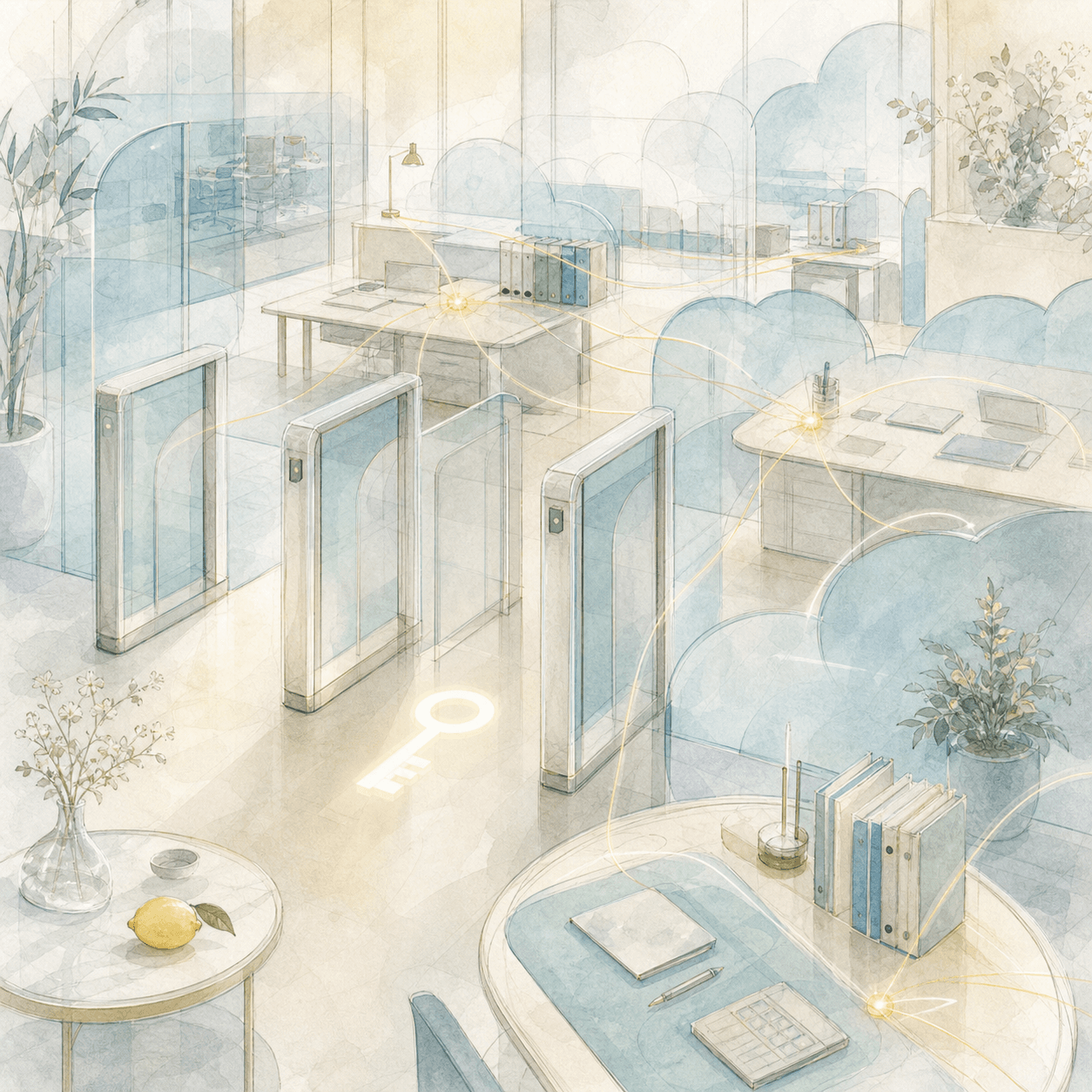

If AI agents enter the enterprise, they may not arrive like strangers walking into the office. They are more likely to grow out of existing office systems, developer systems, security systems, and cloud platforms. They need badges. They need door access. They need logs. They need someone who can stop them.

Microsoft already owns many of those doors.

Products like Microsoft Foundry and Agent 365 should not be viewed only as ordinary product updates. They look more like Microsoft building the company policy layer for future AI workers.

Companies used to manage employee accounts.

Soon, they may also need to manage agent accounts.

That may still sound early, but the direction is clear. A company with a few agents has a small problem. A company with dozens, hundreds, or thousands of agents has a system problem.

Who created them? Who granted permission? What did they read? What did they call? Did they touch sensitive data? Did they spend too much? Did one of them keep moving down the wrong path?

Those answers will not live inside a pretty chat interface. They will live in cloud, identity, security, compliance, logs, and workflow.

In other words, inside the places that often look heavy, expensive, and boring.

Heavy Can Be a Feature

Capital markets love light things: light assets, light teams, light deployment, light growth.

But infrastructure that can absorb enterprise reality is rarely light. It has to hold real business processes. It has to connect with old systems. It has to satisfy legal and security teams. It has to let a CIO sleep at night.

That is why Microsoft's AI investment feels contradictory.

In the short term, it can look unattractive. Money is being spent quickly. The return is not fully clear. Gross margin can face pressure. The market asks for proof, and management has to keep proving.

That discomfort is normal.

But over a longer line, the part of Microsoft that is being criticized may also be the part that is hardest to copy.

Data centers are hard to copy.

Enterprise relationships are hard to copy.

Identity systems are hard to copy.

Office entry points are hard to copy.

Security and compliance are hard to copy.

Making large companies comfortable enough to put AI into workflows is even harder to copy.

Some positives do not arrive wearing a suit. They arrive as invoices, skepticism, and dust.

Microsoft looks like that right now.

The market is looking at the bill. I am more interested in the road rights under its feet.

What Would Need to Go Right

If agents become the next enterprise productivity layer, Microsoft's position could be unusual.

It may not need to own every smartest model.

It needs to become one of the places where enterprises are willing to place agents.

If that happens, Azure is no longer just a compute bill. Microsoft 365 is no longer just an office suite. Foundry, Agent 365, Entra, Defender, Purview, and the wider cloud stack may slowly connect into a network.

That network's value may not be fully priced in today.

It is early.

It is expensive.

And it has not yet turned into a clean profit curve.

But some of the most interesting things in investing sit exactly in places like this.

Everyone can see the cost.

Fewer people are trying to understand the access.

What to Watch

Microsoft does not need more AI headlines. There are already too many headlines, and too much noise.

The important questions are more practical:

- Can Azure demand stay strong?

- Can AI-related revenue keep growing in a measurable way?

- Can Copilot and agents move deeper into enterprise budgets?

- Can cloud gross margin stabilize while AI usage rises?

- Can capital expenditure eventually be digested by revenue?

The market can keep criticizing Microsoft for spending too much on AI.

That is normal.

Sometimes, when a company is accused of burning money, it really is burning money.

Other times, it is building a road before others can see where the road leads.

Microsoft is standing between those two answers.

That is why it remains worth watching.

It has not given the market a certain answer. But it has left a clue: early, deep, and easy to cover with short-term emotion.

If the next stage of AI is just better chat, Microsoft's upside imagination is limited.

If the next stage of AI begins to work inside companies, the hidden road under Microsoft's feet may become wider.

Miss Lemon Note

This is not a buy recommendation or a sell recommendation.

It is only an observation: the market is looking at Microsoft's AI costs with a magnifying glass, but some of those costs may eventually be renamed.

Today, they are called pressure.

Tomorrow, they may be called access.